The Triangle Trade and The Dollar Switchboard

Harrison Mann,

Head of Growth

Before direct-dial telephone networks, placing an international call required an operator. You picked up the receiver, told someone at a switchboard who you wanted to reach, and waited to be patched through. Sometimes this required several intermediate operators in different countries.

This model was pricey and slow, and depended entirely on switchboard availability. Every call went through the same handful of relay points.

In the global FX market, our switchboard is the US dollar.

How the dollar became both gate and gatekeeper

According to the Bank for International Settlements’ 2022 Triennial Survey, the US dollar appears on one side of about 88% of all global FX transactions.

The dollar’s ascent runs through the post-war Bretton Woods agreement, which formally anchored the international monetary system to the dollar. In subsequent decades, US Treasury markets became the world's premier safe asset.

When the Bretton Woods system collapsed in 1971, the dollar lost its formal peg to gold—but retained, and in some ways deepened, its functional centrality to global trade and finance. Dollar-denominated commodity markets, dollar-denominated debt markets, and the dollar’s role in cross-border trade invoicing all reinforced each other, resulting in the system we all know and love.

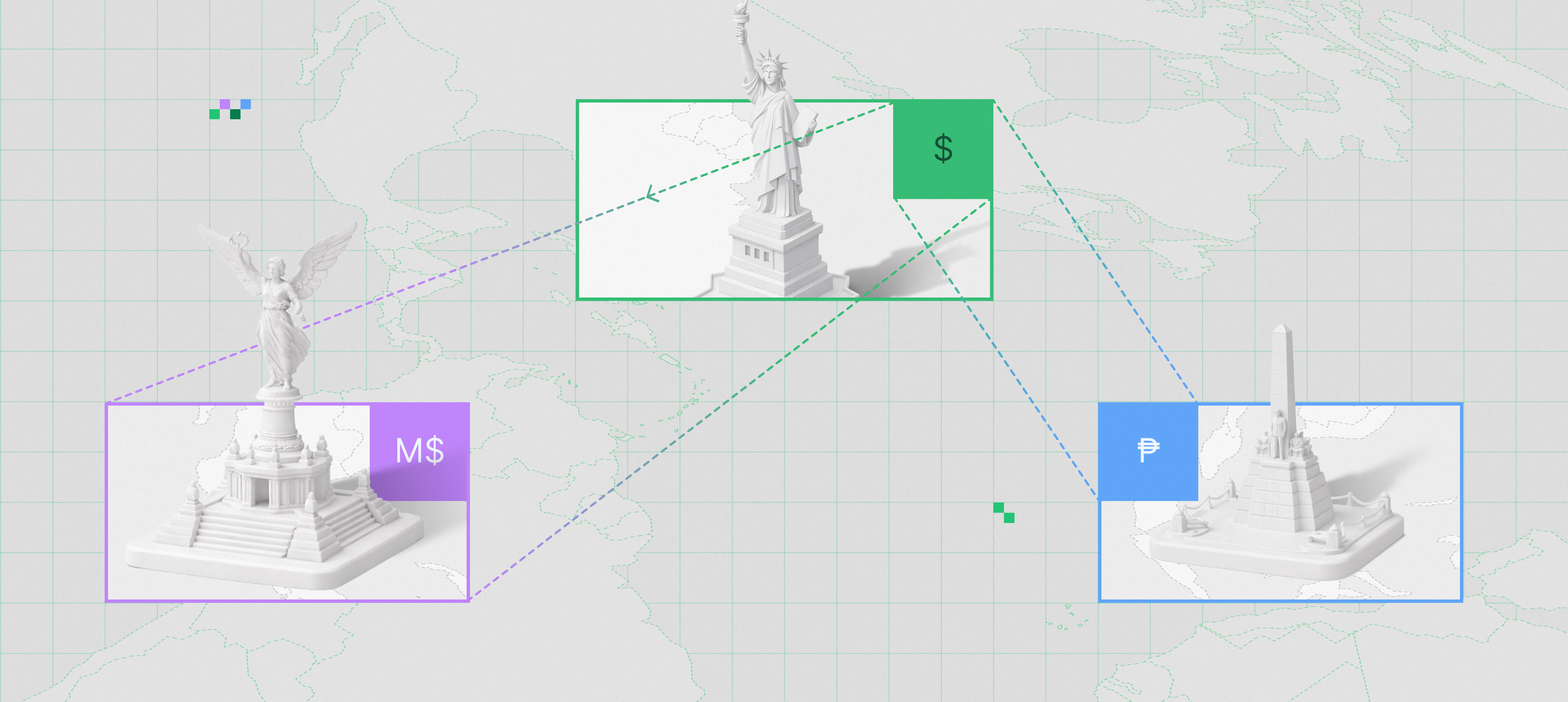

Thus today, if a business in Thailand needs to pay a supplier in Mexico, it ends up executing two transactions: THB/USD, then USD/MXN. The dollar acts as an invisible intermediary in a transaction whose goods and end points may never even touch the United States.

Meet the triangle trade

This routing pattern—dubbed the “triangle trade,” even when more than three parties are involved—is the result of thin liquidity in non-dollar pairs. It happens when there isn’t sufficient natural order flow between currency pairs to support direct exchange, which is actually the case for pretty much every currency pair outside the G7. So a market maker quoting THB/MXN directly needs to warehouse risk in two illiquid currencies simultaneously. The bid-ask spread needed to compensate for that risk is so wide that it’s commercially unattractive to the end customer.

Dollar intermediation solves this problem by concentrating liquidity. Because everyone trades through USD, the USD/THB and USD/MXN books are deep enough to support tight spreads on each leg. The customer gets two efficient transactions instead of one inefficient one. The catch is that two transactions means two spreads, two settlement processes, two sets of counterparty risk, and two times the operational overhead. The efficiency of the individual legs comes at the cost of the efficiency of the whole.

For major currency pairs—EUR/GBP, JPY/CHF—this inefficiency is modest. Direct liquidity exists between these currencies because the bilateral trade flows that generate FX demand are large enough to sustain it. But for most global currency pairs, particularly involving emerging markets, the triangle is the only available route.

Unfortunately for those doing business globally, every basis point of spread on each leg of a triangulated trade represents a real cost—to businesses, to remittance senders, and ultimately to developmental finance. Multiply that across the trillions of dollars that flow through these routes daily, and the aggregate drag on the global economy is substantial.

Stablecoins fix this … right? Right?!

It’s natural to expect that the rise of stablecoins will eventually offer relief from dollar dominance. In practice, the opposite is happening.

Tether’s USDT has become the most traded asset in crypto markets, often surpassing Bitcoin by daily volume. To maintain its peg, Tether holds significant reserves in US Treasury securities. These US Treasury purchases have made it one of the largest holders of short-dated Treasuries globally—a development that means rising stablecoin adoption directly finances US government debt.

In other words, stablecoins in their current form are not an alternative to dollar dominance. A business using USDC to settle a cross-border payment still routes through dollar liquidity.

This is not necessarily a permanent state. Multi-currency stablecoins and algorithmic approaches to cross-currency settlement are active areas of development. But in the near term, the triangle trade is not disappearing—it’s migrating onto new infrastructure while preserving its fundamental structure.

We haven’t replaced the switchboard; it’s just been digitized.

If you’d like to know more about this evolving state of affairs, be sure to read our Q1 2026 report. Chapter 5, “The Dollar Flywheel,” describes how growing stablecoin use doesn’t just increase dollar dependence; it’s also funneling monetary sovereignty away from governments and into privately-held companies.

Share article

Read other articles

Stay informed with our latest articles on currency launches, institutional FX trends, and global liquidity.